The American Dream of home ownership has not disappeared, but for many households it now feels farther away than it did for their parents and grandparents. Fifty years ago, a home could often be bought on a single income with a payment that fit comfortably inside the household budget. Today, even well-qualified buyers frequently find that the monthly payment, the down payment, and the closing costs stretch the limits of what they can afford.

At the heart of the affordability problem: home prices have moved up faster than wages, while everyday expenses have crowded out the savings needed to buy a home in the first place. And when you look back in five-year increments over the last half century, the pattern is hard to ignore. Homeownership has become steadily more difficult to reach.

What changed over the last 50 years?

Housing affordability does not decline in a straight line. It moves with mortgage rates, local supply, household income, taxes, insurance, and construction costs. But the long-term direction is clear: the share of income needed to own a home has risen.

Fifty years ago, housing expense was often around 25% of income. Today, in many markets, the all-in housing payment can reach 40% to 50% of gross household income once mortgage principal, interest, property taxes, and insurance are included.

Here is the broad picture in five-year steps:

- Mid-1970s: Mortgage payments were generally manageable for middle-income households, and it was common to target housing costs near 25% of gross income.

- 1980s: High interest rates made borrowing expensive, even when home prices seemed more reachable than they do today. Monthly payments rose sharply.

- 1990s: Wages improved, but so did expectations. In many areas, buyers still needed two incomes to buy comfortably.

- 2000s: Home values accelerated faster than paychecks, especially in fast-growing regions. Easy credit temporarily hid the problem, but it did not solve it.

- 2010s: Low mortgage rates helped, yet prices recovered faster than wages in many markets. The result was a classic affordability squeeze.

- 2020s: Higher home prices, higher interest rates, and higher insurance and tax bills have pushed monthly ownership costs to levels many buyers did not expect.

In short, the old rule of thumb no longer fits the market. The monthly payment has become a bigger share of income, and the upfront cash needed to buy has become harder to assemble.

Home prices have outpaced wages for decades

The relationship between home prices and wages is the key reason ownership feels more out of reach. Wages have grown over time, but not nearly as fast as the price of buying a home in many places.

That gap matters because housing is not just a sticker price. It is also a mortgage payment, property tax bill, homeowners insurance premium, maintenance reserve, and often homeowners association dues. When prices rise faster than incomes, the entire payment structure becomes harder to support.

In many metro areas today, even a modest home can require a monthly payment that would have bought a much larger property a generation ago. Buyers are often forced to compromise on location, square footage, condition, or commute length. Some are pushed out of ownership entirely and remain renters longer than they planned.

The challenge is even more visible when you compare the old standard of affordability with today’s reality. If housing was once considered affordable at roughly a quarter of household income, then a payment consuming 40% or 50% is not just a little less convenient. It is a fundamentally different burden.

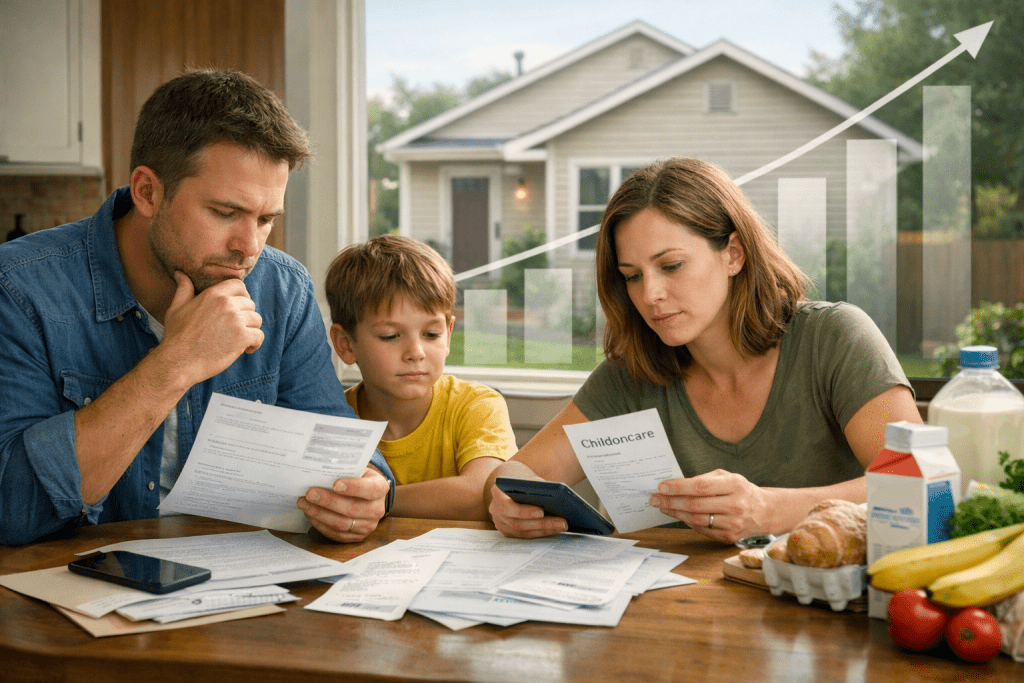

The hidden reason saving for a down payment is harder

Affordability is not only about the mortgage. It is also about getting enough cash together to buy in the first place. That is where modern household budgets feel especially tight.

Fifty years ago, many of the monthly expenses that are now considered normal either did not exist or were rare. Today, they compete directly with the money a family might otherwise save for a down payment.

Monthly expenses that were not part of the typical household budget 50 years ago

- Cell phones and data plans: A family plan can easily run into the hundreds per month.

- Internet service: Now considered essential for work, school, and daily life.

- Child care and daycare: For many families, this is one of the largest monthly expenses outside housing.

- Streaming subscriptions and digital services: Small individually, but significant when added together.

- Home security, app subscriptions, and cloud storage: New recurring costs that did not exist in the same form decades ago.

- Higher transportation costs: Fuel, insurance, repairs, tolls, and longer commutes all chip away at savings.

- Student loan payments: A major barrier for first-time buyers who carry education debt into their 30s and 40s.

- Rising health insurance premiums and out-of-pocket costs: Another unavoidable drain on monthly cash flow.

- Pet care and family support expenses: Increasingly common budget items that compete with home savings.

Even if wages rise, these new and growing monthly obligations can absorb much of the gain. The result is simple: people may be earning more than previous generations, but they often have less left over at the end of the month to save for a home.

Why the monthly payment feels so heavy now

It is important to separate home price from monthly payment. Buyers usually qualify based on the payment, not the sticker price alone. That is why mortgage rates matter so much.

When rates rise, the payment on the same home rises too. A home that seemed barely affordable at one rate can become out of reach at another. Add in higher property taxes, larger insurance premiums, and maintenance costs, and the number can move from “tight but possible” to “not realistic.”

This is one reason many buyers feel trapped. They see a home they might have been able to afford in a different era, but the combination of price, rate, and recurring costs changes the math completely.

Is anything reversing the trend?

There are a few signs that may help over time, but none of them has fully reversed the affordability challenge yet.

Some positive developments to watch

- Wage growth in some sectors: Pay gains can help, though they often lag housing costs.

- More remote and hybrid work: Buyers can sometimes shop in lower-cost markets if they are no longer tied to a downtown office.

- Zoning and land-use reform: Some communities are allowing more starter homes, ADUs, and higher-density housing.

- Down payment assistance programs: State, local, and employer-backed programs can help first-time buyers bridge the gap.

- Alternative ownership models: FSBO, lower-cost brokerage options, and more transparent fee structures can reduce transaction friction.

- More attention to affordability in public policy: Housing supply, permitting, and insurance costs are getting more attention than they did before.

Still, the trend has not truly turned around on a national level. In many markets, new supply remains too limited, land is expensive, labor and materials cost more, and insurance premiums have climbed. The pressure is real, and it is not going away just because demand is strong.

The good news is that buyers today have more information and more tools than buyers did decades ago. They can compare mortgage options, look beyond the most expensive neighborhoods, consider smaller homes, and evaluate alternative buying strategies. Sellers, too, benefit from understanding what affordability means on the other side of the transaction. If buyers are squeezed, demand becomes more selective.

What buyers, sellers, and real estate pros should take from this

For buyers, the message is clear: affordability is no longer about finding a house and getting approved. It is about building a plan that covers the down payment, the monthly payment, and the life you need to live after closing.

For sellers, understanding affordability helps explain why buyers may negotiate harder, why showings may take longer, and why pricing accurately matters more than ever.

For real estate professionals, the market rewards transparency and practicality. Buyers need clear guidance on payment scenarios, not just list prices. Sellers need realistic pricing strategy. And everyone involved benefits when transaction costs are simpler and easier to understand.

Key takeaways

- Homeownership has become less affordable over the last 50 years, especially when measured as a share of income.

- Home prices have generally risen faster than wages, making both monthly payments and down payments harder to manage.

- Modern household budgets include expenses that did not exist 50 years ago, such as cell phones, internet service, daycare, and student loan payments.

- Many buyers now face housing costs that consume 40% to 50% of gross income in high-cost markets.

- There are some signs of relief, including wage growth, remote work, zoning reform, and assistance programs, but the affordability gap remains wide.

FAQ

Why has homeownership become less affordable?

Because home prices, mortgage rates, taxes, insurance, and other ownership costs have risen faster than wages in many places. At the same time, households are carrying more recurring monthly expenses than previous generations.

What is the biggest affordability challenge for first-time buyers?

For many buyers, it is the combination of the down payment and the monthly payment. Saving cash is harder because everyday expenses have grown, and qualifying for a payment is harder because prices and rates are higher.

Are there any signs that affordability is improving?

In some markets, yes. Remote work, wage growth in certain industries, local housing reforms, and down payment assistance programs are helping some buyers. But nationally, the affordability problem is still significant.

What can buyers do in today’s market?

Buyers can get pre-approved early, compare loan options, consider smaller or less expensive neighborhoods, review all monthly costs before making an offer, and look for assistance programs that reduce upfront cash needs.

Final thought

The affordability problem is not just a housing story. It is a household budget story, a wage story, and a supply story. If the next 50 years are going to be different from the last 50, then the market will need more homes, more transparent transactions, and more realistic paths to ownership.

Until then, the best thing buyers, sellers, and real estate professionals can do is understand the numbers clearly and plan accordingly.

Call to action

Like this article? Please share it. Also, register to follow Vohme and receive the latest articles once a week. Vohme – Simply prctical.