Imagine a ballot measure passes and Florida eliminates property taxes tomorrow or even a phased-in program over ten years.. At first glance, it sounds like a huge win for homeowners: no yearly bill, no appeals, no worry about rising assessed values. In reality, property taxes fund core local services—schools, police and fire, roads, trash pickup—and the state and local governments would still need that revenue. Eliminating property taxes would simply shift the bill onto other taxes, fees, service cuts, or new finance mechanisms. This article explains the realistic replacement options, who would gain or lose, and practical steps you can take to measure how such a change would affect your household’s true affordability.

How Florida currently funds local government

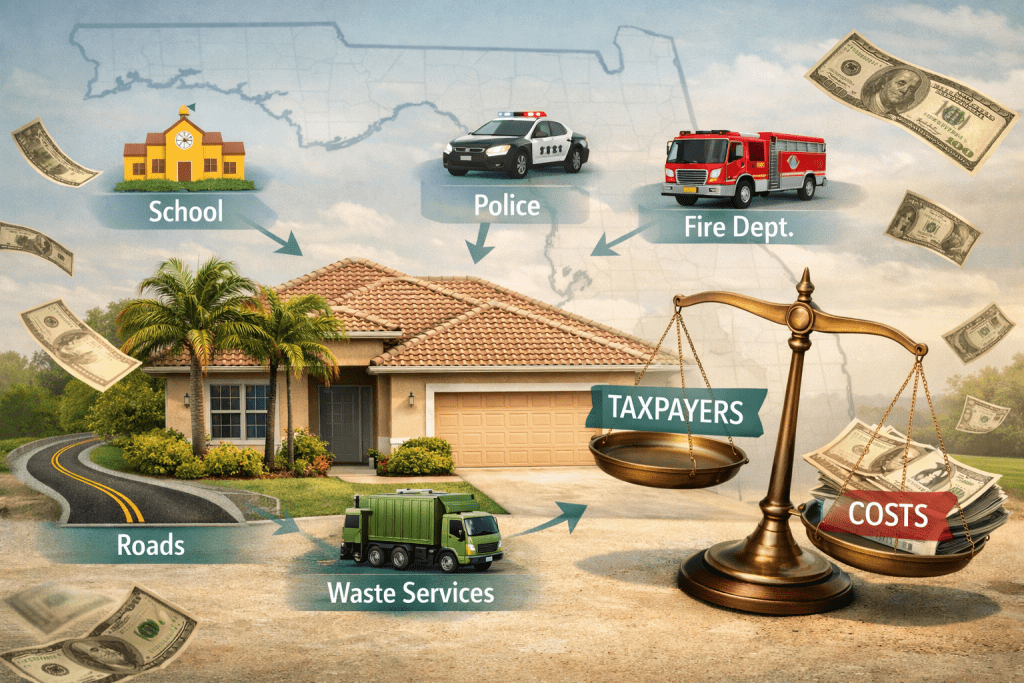

Property taxes are the backbone of local government funding in Florida. Counties and municipalities rely on property tax collections to pay for K–12 public schools (via local levies in cooperation with the state), law enforcement and fire protection, local transportation projects, parks, libraries, and building inspection services. In many jurisdictions, property tax receipts are relatively stable and predictable, which allows for multi-year capital plans and local staff funding.

Florida also uses other revenue streams—sales taxes, tourist taxes, utility fees, impact fees, and state-shared revenue—but those sources typically don’t fully replace the scale and local control that property taxes provide.

What “eliminating property taxes” actually means

Removing the property tax line item does not make government expenses disappear. The key question becomes: How will governments make up the lost revenue?

- They can raise other taxes or fees (sales tax, new state income tax, tourist taxes, utility fees).

- They can shift costs—cut services, defer maintenance, or increase user fees like water and trash.

- They can create special assessments or local service districts that bill property owners directly for targeted services.

- They can borrow (bonds) and defer costs to future taxpayers.

Any combination of these responses will determine the actual winners and losers from a homeowner’s perspective.

How the revenue replacement options would likely hit homeowners

Below are the practical replacement scenarios and how they translate to what homeowners would pay—using simple examples you can adapt to your own numbers.

1) Shift to higher sales tax

One of the politically simplest options is to raise the state or local sales tax. Sales taxes are collected at the point of sale and capture spending by residents and tourists.

Example math: If your household currently pays about $3,000 a year in property taxes, and you spend $40,000 per year on taxable purchases, you would need an additional sales tax of 7.5% (3,000 / 40,000) to break even. If your household spending is lower—say $25,000 per year—the needed increase becomes 12%.

Pros: Revenue can be collected quickly and broadly, including from tourists. Cons: Sales taxes are regressive—they take a larger share of income from lower-income households and seniors with fixed incomes.

2) Introduce a state income tax or local income surtax

Florida currently has no state income tax. Implementing one, or a local surtax, could replace property revenue.

Example math: A household with $60,000 of taxable income that currently pays $3,000 in property tax would face an additional income tax of 5% (3,000 / 60,000) to offset that amount.

Pros: More progressive than sales tax if structured with brackets and exemptions. Cons: Political feasibility is low in Florida and businesses may push back; income taxes can reduce work and investment incentives if poorly designed.

3) New or higher user fees, special assessments, or service districts

Local governments can impose per-parcel fees, increase utility rates, or create fire or stormwater districts with assessments billed to homeowners.

Pros: Keeps a link between services provided and fees collected. Cons: Fees often disproportionately impact homeowners (not tourists or everyday consumers) and can be a flat burden regardless of ability to pay.

4) Cut services or defer maintenance

Governments could reduce service levels—longer emergency response times, larger class sizes, deferred street repairs. These are not taxes but represent reduced public value that homeowners ultimately pay for in quality-of-life impacts and potential property value declines.

5) Increased tourist and business taxes

Raising tourist taxes (hotel taxes) or business taxes shifts part of the burden away from residents to visitors and companies. This helps in coastal Florida markets, but tourist tax revenue is seasonal and volatile.

Who wins and who loses

- Winners: Owners of high-value homes who currently pay large property taxes but have high consumption of tax-exempt goods and can avoid sales-tax-heavy purchases; landlords who can shift costs to renters if market permits; tourists/businesses if taxes shift away from residents.

- Losers: Low-income households and renters facing higher sales taxes or fee hikes; seniors on fixed incomes if homestead protections are removed but sales taxes or fees rise; small landlords if business taxes target property-derived revenue; communities reliant on stable property tax revenue that experience service cuts or deferred infrastructure.

- Neutral/Complex: Middle-income homeowners—impacts depend on household spending patterns, local budget choices, and whether any new tax is progressive or regressive.

Key point: Eliminating property taxes doesn’t eliminate the cost of local government; it only changes who, how, and when people pay for those services.

How to evaluate real affordability impacts for your household

Rather than reacting to headlines, follow these practical steps to estimate how an elimination of property taxes would affect you personally.

- Calculate your current property tax bill. Use your latest county tax bill or mortgage escrow statement to get the exact annual number.

- Estimate your taxable spending. Add up annual purchases that would be subject to sales tax—groceries (if taxed locally), dining, clothing, electronics, home improvement, and services.

- Run replacement scenarios. Use the simple formulas above to see how much a sales tax, income tax, or per-household fee would need to increase to replace your property tax amount.

- Factor in indirect effects. If governments shift to fees or assessments, consider whether your neighborhood would face special service districts that bill only local properties.

- Consider the timing. Taxes can be phased in, and service cuts can compound over time. Check your county’s budget and meeting minutes to see contingency plans.

- Protect cash flow. If you’re close to the margin, model worst-case scenarios and adjust your household budget or emergency fund accordingly.

- Explore tax relief you already have. Verify homestead exemptions, senior exemptions, and any local credits—these matter more if property taxes remain but can also influence how alternative taxes affect you.

Short key takeaways

- Eliminating property taxes would not erase the cost of local services; it would shift revenue collection to other taxes, fees, or cuts.

- The distributional impact depends on the replacement method: sales taxes are regressive; income taxes can be progressive but politically sensitive in Florida.

- Use simple arithmetic (your property tax bill divided by taxable spending or income) to estimate how much other taxes would need to rise for you to be indifferent.

- Homeowners should verify exemptions, run replacement scenarios, and plan for service-level or fee changes that affect cash flow and property value.

Frequently Asked Questions

Would renters benefit if property taxes were eliminated?

Not necessarily. Landlords facing higher non-property taxes or fees may pass costs through to tenants via higher rent. If replacement revenue is raised through sales taxes, renters (who tend to spend more of their income) may be worse off.

Would eliminating property taxes lower home prices?

Possibly. Part of home value reflects the present value of future taxes and local services. If tax structure changes are perceived as unstable or services decline, buyers may discount prices. Conversely, if taxes shift to tourists or businesses, home prices could adjust differently across markets.

How would seniors on fixed incomes be affected?

Seniors often benefit from homestead and senior exemptions. If property taxes are eliminated but replaced by higher consumption taxes or fees, seniors on fixed incomes may be disproportionately harmed because they spend a larger share of income on essentials.

Is a statewide income tax likely in Florida?

Historically, Florida has resisted a state income tax. While not impossible, implementing one would require significant political change or voter approval, making it a less immediate replacement than sales or local fee mechanisms.