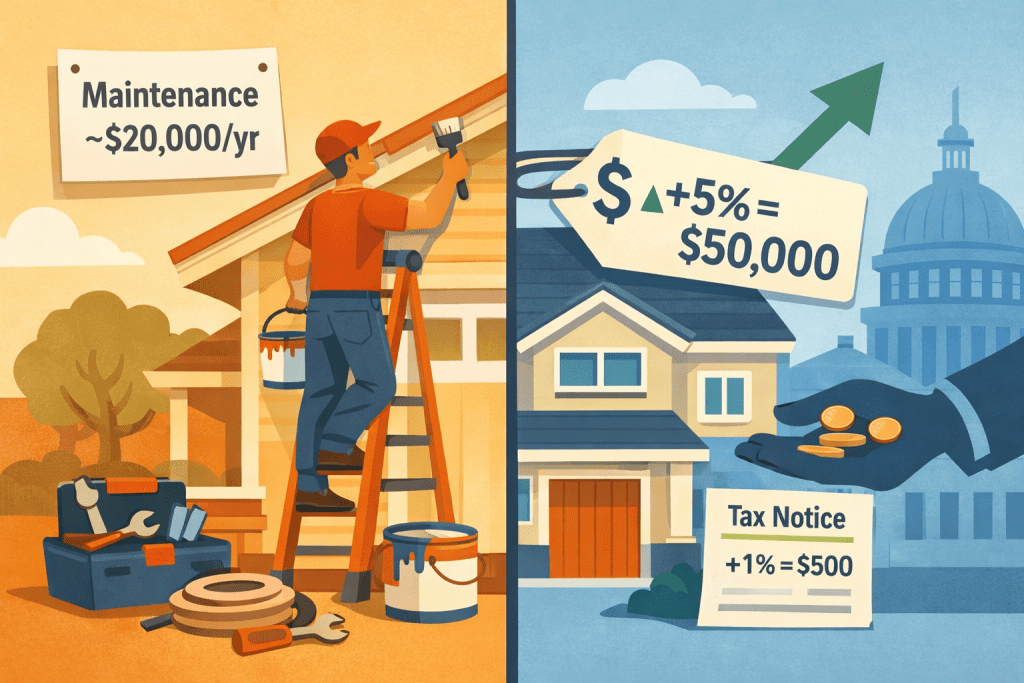

When a neighbor posts on social media that their property tax went up “only 1%” and that they’re comfortable because the home appreciated 5% (about $50,000 on a $1,000,000 house), it can feel like a tidy trade-off. But that shorthand hides a broader mismatch: the homeowner paid roughly 2% of value each year to maintain the house (about $20,000), while the government collects recurring tax increases on the home’s higher assessed value even though the owner only realizes that appreciation when they sell. That gap raises questions about fairness, incentives, and how property taxation shapes local government behavior.

Why this scenario feels unfair

There are three related frictions in the example that lead to the sense of unfairness:

- Cash-flow versus paper wealth: Owners pay real, recurring costs (maintenance, insurance, utilities, financing) in cash year after year. Appreciation is usually paper wealth until a sale converts it to cash. Being taxed on a rising paper value while carrying the cash burden of upkeep creates a liquidity mismatch.

- Asymmetric benefits: The homeowner’s investments in maintenance and improvements often increase the property’s assessed value and thus local tax revenue. The government sees steady revenue growth from those increases whether or not a sale ever occurs.

- Budget incentives: If local government revenue reliably grows with real-estate values, officials may have less incentive to identify efficiencies or cut spending, because rising property values are an automatic revenue engine.

How the numbers work (simple illustration)

Using the scenario’s figures makes the mechanics clear. On a $1,000,000 home:

- 5% appreciation = $50,000 of increased assessed value.

- If the property tax rate is 1% of assessed value, the extra tax on that appreciation is 1% × $50,000 = $500 per year.

- Estimated annual maintenance at 2% = $20,000 in out-of-pocket expense to maintain quality and usefulness.

The homeowner pays roughly $20,000 in upkeep this year and sees a $500 increase in annual property tax liability as a consequence of appreciation. The homeowner only realizes that $50,000 gain if and when they sell the property.

Pros of the current structure

- Stable local revenue: Property taxes provide a relatively predictable source of funding for schools, public safety, streets, and other local services that support property values.

- Benefit link: There’s a conceptual connection between local services and property values—better services often boost demand and prices, so taxing property can be defended as a user/beneficiary charge at the community level.

- Low administrative cost: Compared with income or sales taxes, property taxes are comparatively straightforward to assess and collect using public records and assessments.

- Discourages vacant speculation: Ongoing property taxes impose a cost on holding underutilized land or vacant homes, which can encourage efficient use of housing stock.

Cons and policy concerns

- Liquidity and fairness for fixed-income owners: Seniors or others living on fixed incomes may see taxes rise with market gains even though their cash flow doesn’t. This can force sales, reverse mortgages, or tax deferrals.

- Disincentive for improvements: Owners may hesitate to invest in upgrades if those improvements are likely to increase assessed value and future taxes, particularly if they don’t plan to realize the value soon.

- Revenue-driven spending: When local budgets grow with rising property values, governments may expand services or staffing in ways that are hard to roll back during downturns, making municipal finances pro-cyclical.

- Regressive impacts: While rich homeowners may absorb higher taxes more easily, middle-income owners can feel a disproportionate burden—even if the tax is a small percentage of the home’s value—because it affects operating budgets and monthly affordability differently.

- Assessment lags and volatility: Some jurisdictions reassess infrequently or with lags; others treat recent sales as triggers. The mechanics can produce inconsistencies and unexpected tax shocks.

Policy approaches and alternatives

Several policy tools try to smooth these tensions. Each has trade-offs:

- Assessment caps (e.g., Prop 13-style limits): Cap annual increases in assessed value. Pros: predictability and protection for long-term owners. Cons: can shift the tax burden to newer buyers and reduce revenue responsiveness.

- Homestead exemptions and circuit breakers: Target relief at low- and fixed-income owners. Circuit breakers limit tax payments relative to income. Pros: fairness for vulnerable households. Cons: increased complexity and cost to administer.

- Tax deferral programs: Allow qualifying homeowners to defer taxes until sale or transfer. Pros: fixes liquidity mismatch. Cons: accrues liens and interest; deferrals must be repaid eventually.

- Split-rate taxation: Tax land and improvements at different rates (or tax land more heavily). Pros: discourages speculation and rewards productive improvements. Cons: politically difficult and requires valuation adjustments.

- Targeted grants or credits: Subsidies for maintenance or energy retrofits that reduce the need for owners to bear full upfront costs. Pros: encourages upkeep without penalizing owners with higher future taxes. Cons: requires public funding and program oversight.

Practical steps homeowners can take

Whether you agree with the system or not, there are concrete actions to protect your cash flow and minimize surprises:

- Know your assessment and appeals process: Review your property tax assessment each year. If values seem wrong, file an appeal before the deadline.

- Check for exemptions: Seniors, veterans, people with disabilities, or primary-residence owners may qualify for exemptions or lower assessed values.

- Document improvements: Keep records of permitted work and assess whether improvements are likely to materially affect assessed value. For some projects, the value added may be less than the cost.

- Budget for maintenance: Treat routine upkeep as a necessary annual cost—2% is a common rule-of-thumb for higher-value homes—and include it in your cash-flow planning.

- Consider deferral options: If you qualify, property tax deferral programs can be a tool to avoid forced sales for cash-constrained owners.

- Plan before major upgrades: Weigh the expected increase in market value against the additional taxes you may owe and the timing of when you’ll realize the gain.

Key takeaways

- Property taxes convert paper gains into recurring revenue for governments; homeowners often bear large cash costs for maintenance long before they realize appreciation.

- The system provides stable local funding but creates liquidity and incentive mismatches that can be unfair to fixed-income and middle-income owners.

- Policy tools (caps, exemptions, deferrals, targeted credits) can mitigate harm but introduce trade-offs and complexity.

- Proactive homeowner steps—appeals, exemptions, budgeting, and program awareness—are practical ways to manage the impact.

Frequently asked questions

Q: Am I taxed on unrealized gains every year?

A: Generally you pay tax on the assessed value of your property each year, not on realized gain. If assessed value rises with market prices, your annual property tax bill will typically increase even though the gain isn’t cashed out until a sale.

Q: Can I avoid higher property taxes after making home improvements?

A: Not always. Significant improvements can trigger reassessment and higher taxes. Some minor repairs do not increase assessed value materially, but permitted additions or capital improvements usually have an effect. Evaluate costs versus likely value added before proceeding.

Q: What relief options exist for people on fixed incomes?

A: Many jurisdictions offer homestead exemptions, senior exemptions, circuit-breaker credits, or tax-deferral programs. Eligibility rules vary—check with your county assessor or tax office.

Q: Do rising property taxes mean local governments are being wasteful?

A: Rising tax revenue is not proof of waste. But when revenue automatically grows with property markets, it can reduce political pressure to find efficiencies. Oversight, budgeting discipline, and transparent capital planning matter.

Q: Should I factor future property-tax increases into my decision to renovate or sell?

A: Yes. Renovation may raise taxes if it increases assessed value, and selling crystallizes previously unrealized gains (and may trigger capital gains taxes). Factor both into the financial plan and speak with a tax advisor if needed.

Call to action

Curious how taxes, maintenance, and selling costs affect your net proceeds? Contact Vōhme to get a clear, low-cost estimate of your home’s selling scenario and learn options that help you keep more of your equity.